Weekly|Why Memory / CPU Rally Accelerated and Outperformed Optics, SMTC & AMD Deep Dive, DDOG, APP, LITE, COHR, PLTR, NET, RKLB, RDW

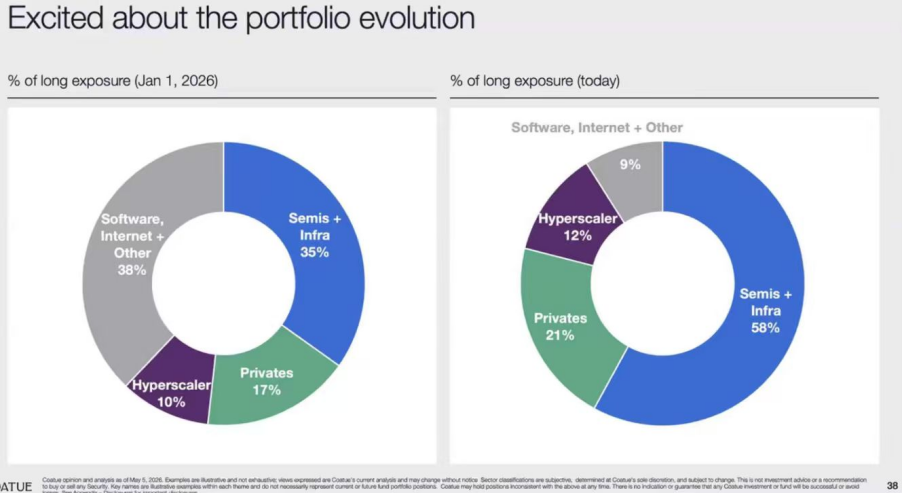

A week dominated by tons of earnings reports and a relentless rally in AI semis, especially memory and CPU stocks. As our long-term readers would recall, we have consistently highlighted the “mis-positioning” by many US funds, which significantly underweight semi/hardware while overweighting software/internet, and, more importantly, they are starting to adjust. This was confirmed by Coatue’s latest presentation, in which they disclosed that Semis + Infra’s long exposure % jumped to 58% as of late, up from 35% at the beginning of the year. This is at the expense of Software, Internet + Other exposure decreased materially.

Source: Coatue

Meanwhile, Altimeter’s Brad Gerstner openly justified the valuation of memory stocks and said he will be on a podcast with the Micron CEO in a few weeks to discuss how the shortage could last until 2028/29 or even longer, suggesting a material shift in his fund’s positioning, too. We sense that the attitude change by these two reputable US TMT funds has ignited FOMO among other investors, including both HFs and LOs, thereby accelerating stock moves lately.

Under this assumption, we think the performance gap between memory/CPU and optics is explanatory. For these funds that missed out on the AI semi rally largely since 2023, MU/SNDK and INTC/AMD are at least names they have known for years, compared to LITE/COHR, which were smaller in market cap and more difficult to understand from a technology perspective. Moreover, MU/SNDK’s lower valuation multiples on paper are a big help. We believe the LTA announcement during SNDK earnings gave the funds we mentioned above a major reason to chase the names here. The market is starting to discuss that once LTAs exceed 50% of the mix, the stock can no longer be viewed as cyclical. We are increasingly hearing investors benchmarking NAND valuation to HDD at 8-10x FCF. You’ll probably recall the LTA Report we published—the first in-depth LTA Report in the market —which laid out the case for why this LTA cycle is different from previous ones.

In general we have been long in all three AI beneficiary segments and would suggest investors exercise caution in names that are going vertical in the near term, while paying closer attention to other areas that are being neglected. On the Premium Research side, we published an SMTC initiation and an AMD deep dive, among others, validating our conviction in all these segments. Please contact sales@funda.ai for more information.

This Week’s Reports

Review|DDOG 1Q26: Big Guidance Upside Surprise, No Growth Cliff Concern Anymore. We were bullish into the event but earnings were even stronger than our higher-than-consensus estimates. 1Q26 met expectations but the real story was the guide — 2Q26 +30% YoY (implying ~35% with the typical 5pt beat) and FY26 raised to 26-27% (low-to-mid 30s on actuals), effectively retiring the 2H OpenAI cliff narrative. Two new hyperscaler AI training wins reinforce DDOG’s tech moat over in-house and OTel alternatives.

Review|APP 1Q26: Management Guides E-commerce to ~20% of US Revenue, +25% QoQ. Revenue +59% YoY in line; the more important read is the explicit 2Q26 guide of e-commerce +25% QoQ with April marking a record month — exactly tracking our Preview’s +23% bogey. With European GA in June and CTV emerging as a first-time upside contributor, the e-commerce ramp is clearly inflecting and gaming shows no deceleration.

Review|RDW 1Q26: Headline Miss, Clean Margins, Prime Optionality. Revenue grew 58% YoY but missed by 7%, with after-hours weakness driven by the $350M ATM rather than the print itself; underneath, GM expanded to 26.6%, backlog hit a record $498M, and book-to-bill was 1.92x. Andromeda (~$6B opportunity), Golden Dome (VLEO/GEO prime), and Lunar Power Grid reframe RDW from components supplier toward space infrastructure prime — the dilution is buying optionality, not survival.