Deep|SPCX: S-1 Analysis

Executive Summary

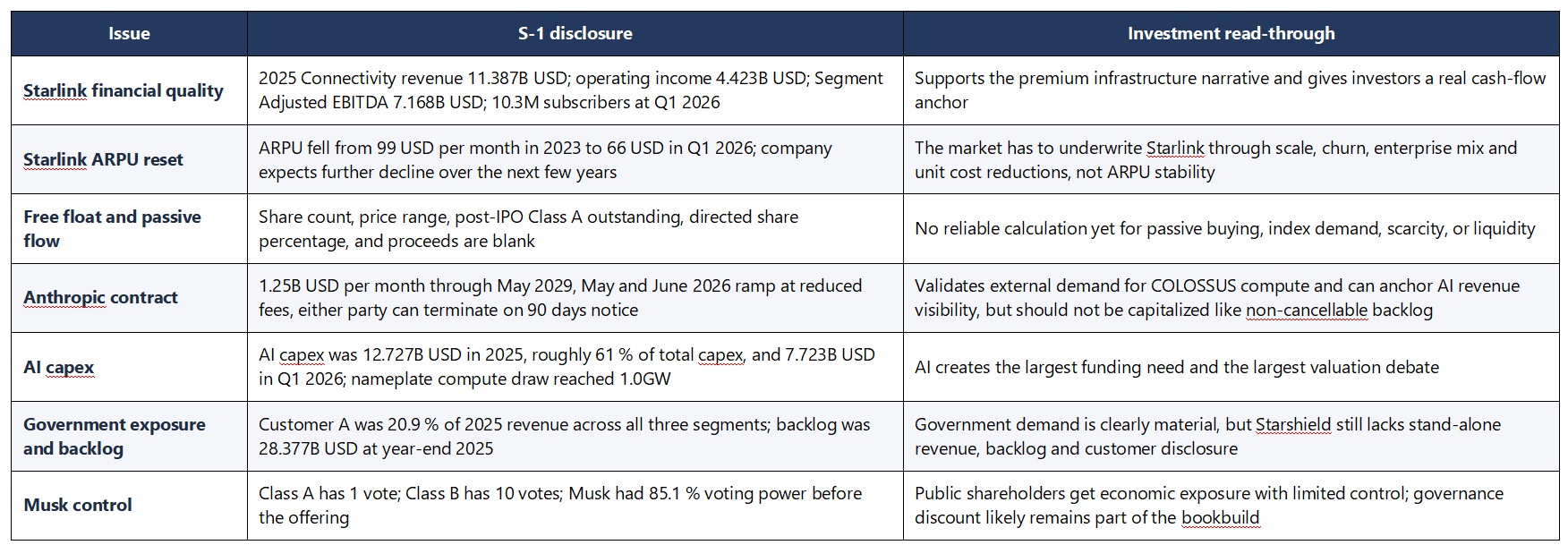

SpaceX should be framed first as a float-black-box and AI-infrastructure IPO, not a clean Starlink listing. The cover page still leaves shares offered, price range, post-IPO Class A outstanding, directed share allocation and proceeds blank, so hedge funds cannot yet calculate free float, passive demand, index flow, borrow or first-day liquidity. Behind that trading setup, the real S-1 surprises are the Starlink ARPU reset from 99 USD per month in 2023 to 91 USD in 2024, 81 USD in 2025 and 66 USD in Q1 2026, with the company indicating further decline; the May 2026 Anthropic cloud services agreement that can reach 1.25B USD per month through May 2029, or 45B USD over 36 months before ramp and termination adjustments; AI capex of 12.7B USD in 2025, roughly 61 % of company capex, plus 7.7B USD in Q1 2026 alone; Bastrop being positioned to produce AI compute satellites for 2028-plus orbital deployment; Blue Origin TeraWave being named in the competitive set; the Cursor equity option potentially representing a 60B USD strategic outlay if exercised; Starshield disclosure remaining unusually thin; and Musk’s 366-day lock-up covering his shares with no early release.

The first-order issue for hedge fund investors is not whether SpaceX has strategic scarcity. It does. The issue is that the preliminary S-1 still leaves out the share count and float data required to model the first-day technical setup. Class A shares offered, price range, post-IPO Class A outstanding, directed share percentage, net proceeds, and post-IPO voting percentages are all blank. Until the S-1/A fills those fields, free float, float-adjusted market cap, index eligibility, ETF demand, passive flow, borrow availability, and day-one liquidity cannot be underwritten with confidence.

The most important new business disclosure is the Anthropic cloud services agreement. SpaceX disclosed that Anthropic agreed to pay 1.25B USD per month through May 2029 for access to compute capacity across COLOSSUS and COLOSSUS II, with May and June 2026 ramping at reduced fees. The contract reframes part of the AI capex burden as external merchant compute infrastructure rather than purely internal Grok training spend. The offset is that either party may terminate on 90 days notice, and the S-1 does not disclose gross margin, minimum commitment mechanics, utilization, or capacity allocation.

Connectivity is the investable core today. It includes Starlink Broadband, Starlink Mobile and government connectivity including Starshield, although Starshield is not separately broken out. Connectivity generated 11.387B USD of revenue in 2025 and 7.168B USD of Segment Adjusted EBITDA, implying roughly 63.0 % margin and roughly 3.0B USD of segment cash generation after capex. The disclosure supports the view that Connectivity is already a scaled cash generator. The missing pieces are still material: no consumer churn, no detailed split across maritime, aviation, government, Starshield, and direct-to-device, and ARPU declined from 99 USD per month in 2023 to 66 USD per month in Q1 2026. The offset is that enterprise retention is unusually strong: since 2023, no Starlink Enterprise customer contributing more than 750,000 USD of annual revenue has voluntarily discontinued service.

The governance discussion will matter more than usual. Musk had 85.1 % combined voting power before the offering, Class B shares carry 10 votes per share, and Class B holders have the right to elect a majority of the board. Traditional long-only governance teams, public pension funds, and old-line Wall Street committees can still participate in the deal, but this structure gives them very little control after purchase. That should create a governance discount unless the float is extremely tight or the IPO is priced with enough concession.

What Matters For Pricing

Source: SpaceX S-1 filing

Business Mix And Segment Structure

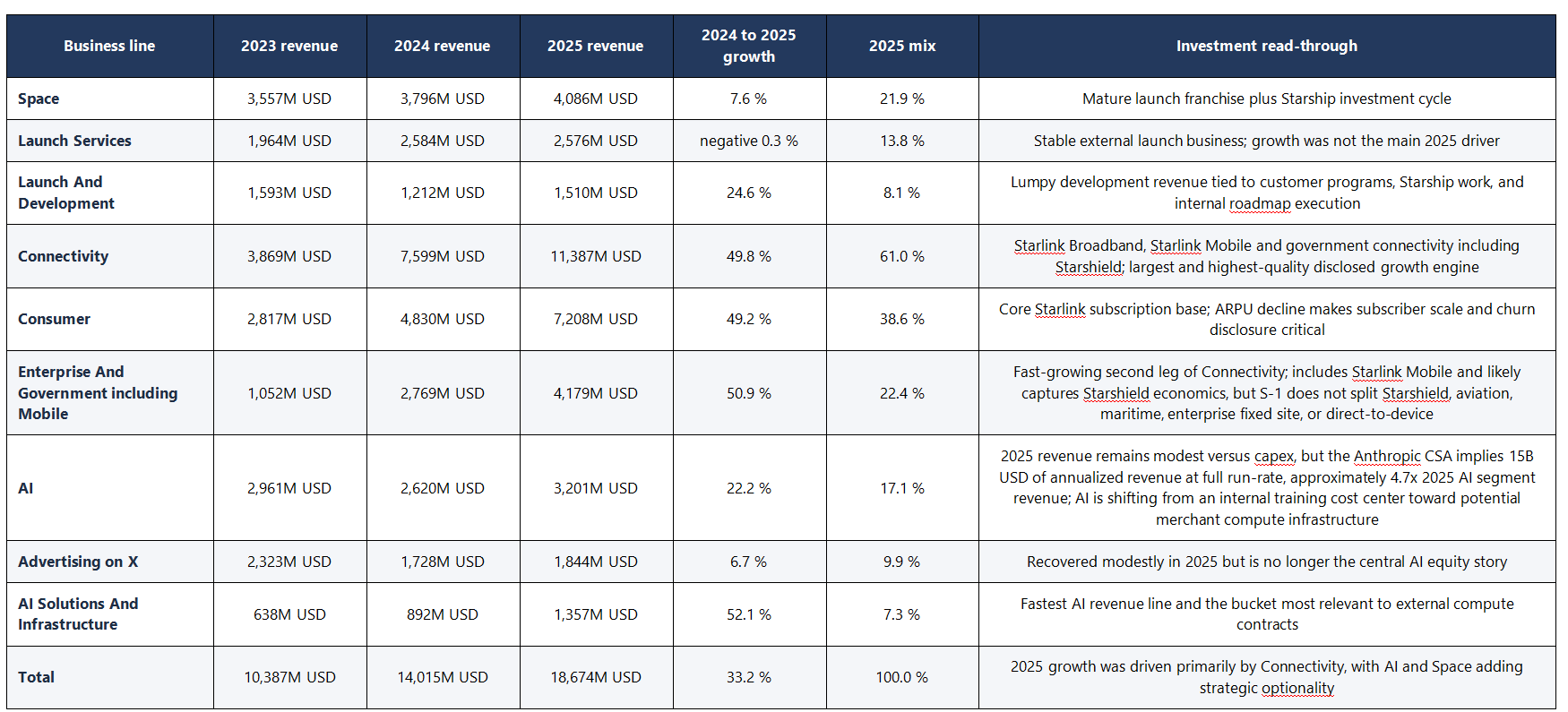

SpaceX has three disclosed revenue segments: Space, Connectivity, and AI. The mix matters because this is not a single-profile operating company. Connectivity is already the largest segment and the main cash-flow anchor. Space is strategically essential but was not the primary 2025 growth driver. AI is smaller in reported revenue but carries the largest capex burden and the largest narrative swing after the Anthropic disclosure.

Source: SpaceX S-1 filing

Connectivity is the core engine and should be read as Starlink Broadband, Starlink Mobile and government connectivity including Starshield, even though the S-1 does not provide a separate Starshield revenue split. The segment generated 11.387B USD of revenue in 2025, 61.0 % of company revenue, and grew 49.8 % year over year. It added 3.788B USD of revenue from 2024 to 2025, or roughly 81 % of SpaceX consolidated revenue growth. Starlink has already moved far beyond being an adjacency to launch. It is now the main business, more than four times Launch Services revenue and almost three times total Space segment revenue.Enterprise And Government is the high-value growth pocket inside Connectivity. Revenue grew from 1.052B USD in 2023 to 2.769B USD in 2024 and 4.179B USD in 2025, nearly quadrupling over two years. That growth likely reflects a mix of Starshield, aviation, maritime, enterprise fixed-site and mobile use cases. The issue is not demand quality; it is disclosure quality. The S-1 still does not split Starshield, aviation, maritime, enterprise and direct-to-device, which means investors cannot yet assign the right mix of defense, mobility and enterprise multiples.

Launch Services is effectively flat. Revenue was 2.576B USD in 2025 versus 2.584B USD in 2024, a 0.3 % decline. That supports the same conclusion we laid out in our prior SpaceX trilogy: Falcon 9 is a proven franchise, but the launch services revenue line is near its mature run-rate unless Starship opens a new capacity and cost curve. Space remains strategically essential because it enables Starlink V3, Starlink Mobile, national security payloads and future orbital infrastructure, but the near-term revenue acceleration is not coming from Falcon launches.

AI is a material drag on reported profitability, but the accounting requires care. The AI segment had 3.201B USD of 2025 revenue and a 6.355B USD operating loss, while AI capex reached 12.727B USD. However, xAI was formally combined in February 2026, so the 2025 AI segment history is a retrospective common-control recast rather than a normal standalone operating history at SpaceX. That makes trend interpretation messy: the losses are real for pro forma economics, but investors should not read 2025 as a clean year of post-integration operating performance.

Advertising on X is not the recovery story. Revenue was 1.844B USD in 2025, up only 6.7 % year over year and still well below pre-Musk acquisition levels. The more relevant AI revenue line is AI Solutions And Infrastructure, which grew 52.1 % to 1.357B USD in 2025 and should be the bucket most exposed to the Anthropic cloud services agreement. The investor question is whether that line can become a real merchant compute revenue stream large enough to offset the scale of AI capex.